A contract with a handshake is valid

Managing director Tina Gerfer of Wilhelm Rasch Spezielmaschinenfabrik has modernised the company and successfully guided it through difficult times.

Read more "

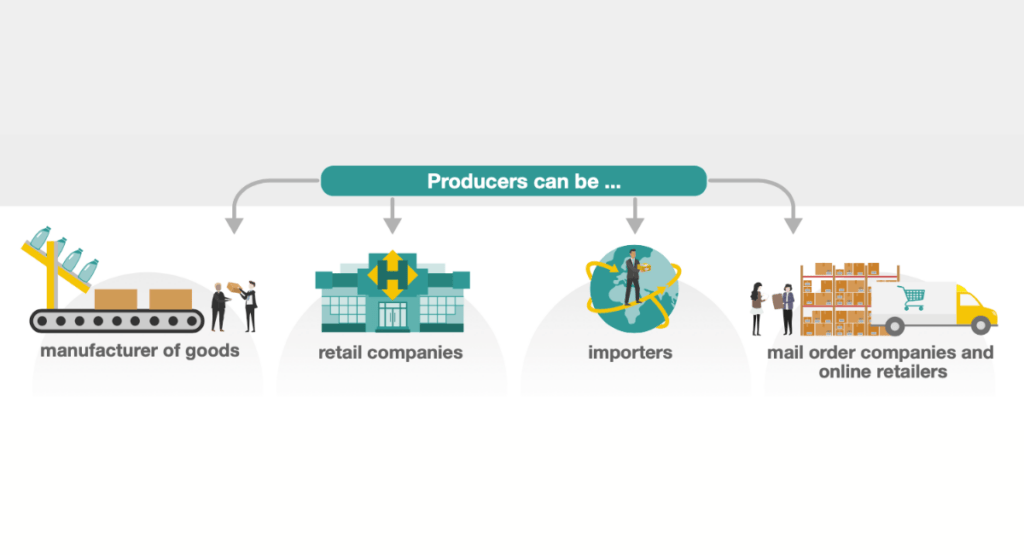

According to the Packaging Act (VerpackG), all companies that commercially market goods in Germany are obliged to register in the LUCID packaging register, regardless of the type and quantity of packaging. In addition to producers, this can also include trading companies, importers of packaged goods or mail-order and online traders if all the requirements apply.

Licensing agreements must be concluded for the expected packaging volumes for their disposal. According to the current state of knowledge, it is estimated that of the 300 relevant top companies, about ten per cent will conclude or have concluded contracts for two years. However, the vast majority of the obligated (six-digit number of) companies circulate such small quantities of packaging that it does not seem to have been worthwhile for these companies to deal with this legally complex issue anew every year. This also applies to customers with micro-circulation contracts, who often conclude their contract online.