A new report on the global market for bio-based polymers forecasts annual growth of 17 per cent between 2023 and 2028. Rising demand in Asia and the USA is driving growth, although Europe's share of the global market has declined.

The year 2023 was a promising year for bio-based polymers: while the PLA capacities increased by almost 50 per cent, polyamide capacities and epoxy resin production are also showing steady growth. Capacities for 100 per cent bio-based PE were also expanded. PE and PP made from bio-based naphtha continued to establish themselves with growing volumes. Current and future expansions for PHAs are still being planned.

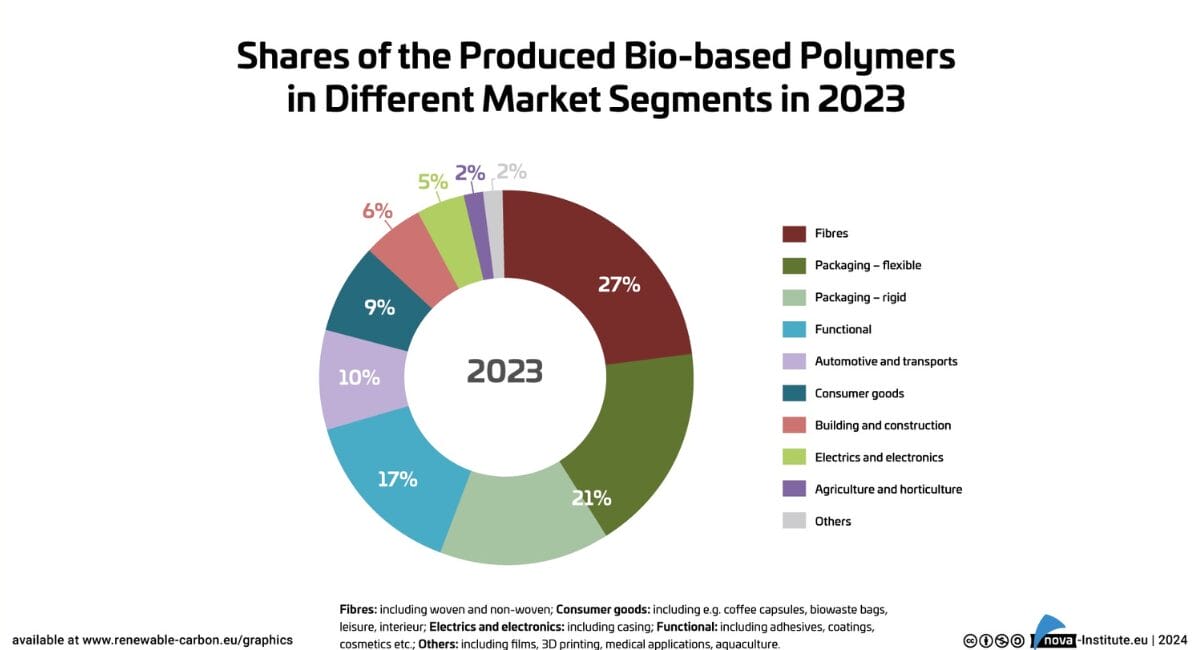

In 2023, the Production volume of all bio-based polymers around 4.4 million tonnes and thus corresponds to 1 per cent of the production volume of fossil-based polymers. At 17 per cent, the compound annual growth rate (CAGR) for bio-based polymers is significantly higher than the overall growth of the polymer market (2-3 per cent) - this trend is expected to continue until 2028.

The new market and trend report „Bio-based Building Blocks and Polymers - Global Capacities, Production and Trends 2023-2028“, written by the international biopolymer expert group of the nova-Institute, calls Capacities and production data for 17 commercially available bio-based polymers in 2023 and also includes a forecast for 2028. The report is now available in full.

Brands strengthen commitment

Some global brands are already expanding their raw material portfolios and, in addition to fossil carbon, are also sourcing renewable carbon, CO2, recycling and, in particular, biomass, resulting in a Increase in demand for bio-based and biodegradable polymers leads. At the same time, the necessary political support is lacking, particularly in Europe, where only biofuels and bioenergy continue to be subsidised. The situation is different in Asia and the USA, where supportive legislation is driving demand.

In 2023, Asia will have 55 per cent of the has the world's largest installed bio-based production capacities, making it the leading continent. It has the largest capacities for PLA and PA, among others. North America accounts for 19 per cent, with large installed capacities for PLA and PTT, while South America's share is 13 per cent and is primarily based on PE. The European share of global capacity for bio-based polymers fell to just 13 per cent compared to 2022.

This is mainly based on the updated data for PE and PP produced in Europe, where only 10 per cent of the total volume is bio-based. 90 per cent is „bio attributed“ on the basis of „Mass Balance and Free Attribution (MBFA)“. The European share is determined in particular by the installed capacities for SCPC and PA. Less than 1 per cent of Australia/Oceania's share is based on SCPC (Figure 8). With an expected CAGR of 35 per cent between 2023 and 2028, the share of Asia has by far the highest growth rate compared to other regions of the world in the area of bio-based polymer capacities. This increase is primarily due to expanded production capacities for PA, PHA and PLA.

The annual European Bioplastics and from Plastics Europe The data published in this report is taken from the nova Institute's market report, albeit with a smaller selection of bio-based polymers and application areas.

Source: nova-Institute